1 INSIGHT

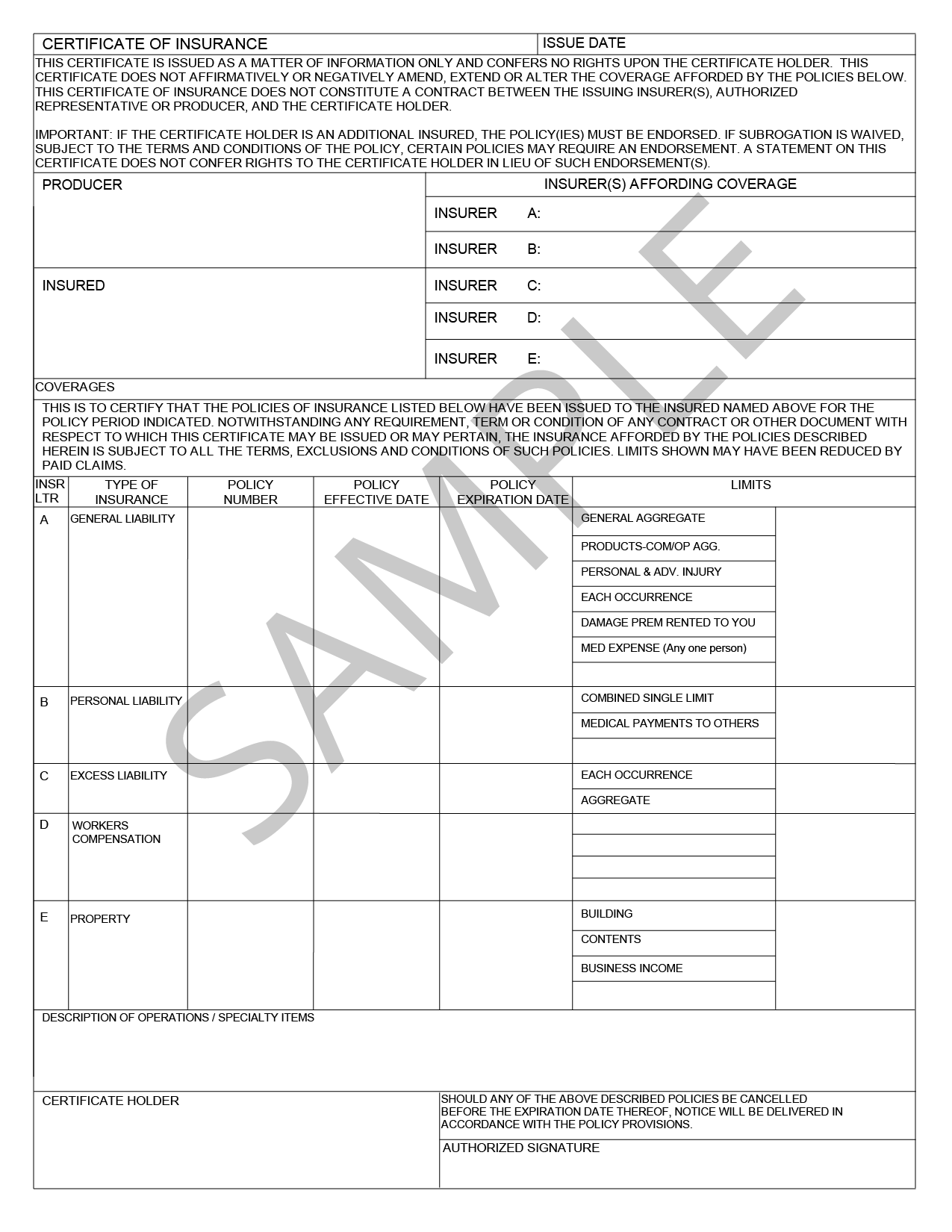

Before moving into an industrial building, tenants must meet the lease’s insurance requirements and provide a valid Certificate of Insurance (COI).

Landlords require specific coverage types and limits, and proof must be provided through a COI before keys are released. Missing endorsements or incorrect language can hold up move-in and even put the tenant in default.

Insurance compliance is a critical step in securing possession of your industrial space.

2 ACTION STEPS FOR TENANTS

- Review Insurance Requirements Early

Confirm required coverage, including:

– Commercial General Liability (CGL)

– Property Insurance

– Workers’ Compensation

– Auto Liability (if applicable)

– Umbrella / Excess Liability

Check coverage limits and required endorsements (e.g., additional insured, waiver of subrogation). - Verify Insurance Provisions With Your Broker & Insurance Agent

Ensure the following:

– The COI lists the landlord and/or property manager correctly (ask the listing agent or landlord which name and address should appear on the COI)

– The COI lncludes required endorsements

– Tenant verifies policy limits per lease liability insurance requirements (e.g., $2,000,000 per occurrence, $4,000,000 aggregate)

– The COI is delivered and approved by Landlord before taking possession of the space

Small wording errors can delay occupancy.

3 KEY TAKEAWAYS

- Insurance compliance is required under most industrial lease agreements.

- A COI must reflect the lease terms precisely.

- Working with your insurance agent in advance reduces the risk of occupancy delays.